How to Calculate AMT: A Step-by-Step Guide to Minimize Tax Stress

Rohit Kapoor

Rohit Kapoor

Calculating taxes can be complicated, especially when the Alternative Minimum Tax (AMT) comes into play. If you’ve ever found yourself wondering how AMT works, or whether it applies to you, you’re not alone. This step-by-step guide will break down the process of calculating AMT into simple, actionable steps, ensuring you’re informed and prepared.

The Alternative Minimum Tax (AMT) is a parallel tax system designed to ensure that high-income earners pay a minimum amount of taxes, regardless of deductions or credits. While the intention behind AMT is fair, its complexity can leave taxpayers scratching their heads. This guide explains everything you need to know about calculating AMT, from understanding its basics to a detailed walkthrough of the calculation process.

What is AMT?

AMT stands for Alternative Minimum Tax. It’s a tax system created to prevent high-income earners from using excessive deductions and loopholes to reduce their tax liability to near zero. Essentially, AMT ensures that everyone pays their fair share.

Unlike regular taxes, which are based on your taxable income and deductions, AMT operates on a modified set of rules. These rules often disregard common deductions, leading to a higher taxable income base.

Who Needs to Worry About AMT?

Not everyone has to deal with AMT, but certain factors can trigger it. Here’s what you need to know:

- Income Thresholds: AMT is more likely to affect taxpayers with higher incomes, typically those earning above $200,000 annually.

- Common Triggers:

- High state and local tax deductions

- Exercising incentive stock options

- Large miscellaneous itemized deductions

- High income with multiple dependents

If your financial situation includes any of these triggers, it’s essential to check whether AMT applies to you.

How Does AMT Differ From Regular Tax?

The key difference between AMT and regular taxes lies in how income and deductions are calculated. Here are some distinctions:

|

Aspect |

Regular Tax |

AMT |

|

Deductions Allowed |

Many itemized deductions allowed |

Many deductions disallowed |

|

Tax Rates |

Progressive (10%-37%) |

Flat rates (26% or 28%) |

|

Adjustments and Credits |

Broadly applicable |

Restricted adjustments/credits |

By removing certain deductions and applying different rates, AMT often results in a higher tax bill for affected individuals.

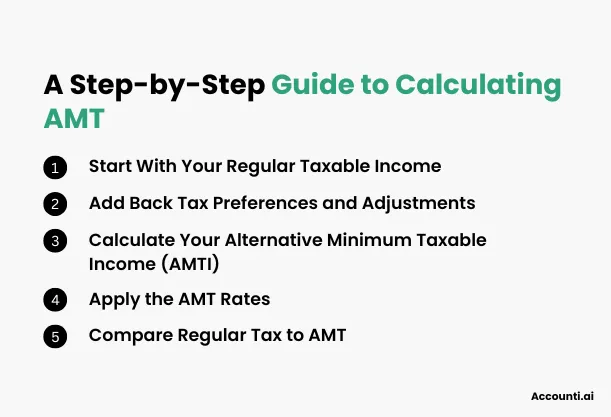

A Step-by-Step Guide to Calculating AMT

Calculating AMT might sound daunting, but breaking it into steps simplifies the process. Let’s dive into each step:

Step 1 - Start With Your Regular Taxable Income

Begin by determining your taxable income as you would for your regular taxes. This includes:

- Summing up all sources of income (wages, dividends, interest, etc.).

- Subtracting allowable deductions, such as standard deductions or itemized deductions.

This regular taxable income serves as the starting point for AMT calculations.

Step 2 - Add Back Tax Preferences and Adjustments

AMT calculations require adding back certain deductions and preferences that are disallowed under AMT rules. These include:

- State and Local Tax Deductions: Amounts deducted for state and local taxes are added back to your income.

- Miscellaneous Deductions: Any miscellaneous itemized deductions must also be added back.

- Incentive Stock Options (ISO): The spread between the grant price and exercise price is added as income.

- Standard Deduction: If you claimed the standard deduction for regular taxes, it must be added back for AMT purposes.

Step 3 - Calculate Your Alternative Minimum Taxable Income (AMTI)

Once you’ve adjusted your regular taxable income by adding back preferences and adjustments, you arrive at your Alternative Minimum Taxable Income (AMTI). This is the income base used for AMT calculations.

- Apply AMT Exemptions: AMT allows for exemptions based on your filing status:

- Single: $81,300 (2024)

- Married Filing Jointly: $126,500 (2024)

- Married Filing Separately: $63,250 (2024)

However, these exemptions phase out at higher income levels. If your AMTI exceeds certain thresholds, the exemption amount is gradually reduced.

Step 4 - Apply the AMT Rates

AMT has two flat rates: 26% and 28%.

- Apply the 26% rate to the first $220,700 (2024) of AMTI.

- Apply the 28% rate to any amount above $220,700.

For example, if your AMTI is $300,000:

- The first $220,700 is taxed at 26%.

- The remaining $79,300 is taxed at 28%.

Step 5 - Compare Regular Tax to AMT

Finally, compare your AMT liability to your regular tax liability. If your AMT is higher, you’ll pay the difference as an additional tax. If it’s lower, you’ll pay only the regular tax amount.

Tools and Tips for Calculating AMT

Using Tax Software

Tax software can automate the complex AMT calculations. Popular platforms like TurboTax and H&R Block have built-in features to calculate AMT based on your inputs. These tools:

- Automatically identify triggers

- Add back preferences and adjustments

- Compare AMT and regular tax liabilities

Consulting a Tax Professional

If your financial situation is complex, it’s worth consulting a tax professional. They can:

- Identify AMT triggers specific to your income and deductions

- Offer strategies to minimize AMT liability

- Ensure compliance with all tax laws

Tips to Minimize AMT Liability

While AMT can’t always be avoided, proper planning can reduce its impact. Here are some tips:

- Time Your Deductions: Shift deductible expenses to years when AMT doesn’t apply.

- Monitor Incentive Stock Options: Plan the timing of stock option exercises to avoid triggering AMT.

- Review Your Investment Strategy: Reduce reliance on private activity bonds, as their interest is taxable under AMT.

Conclusion

Calculating AMT doesn’t have to be intimidating. By understanding the rules, following the steps outlined in this guide, and using available tools or professional help, you can ensure compliance and potentially minimize your AMT liability. Remember, knowledge is power when it comes to taxes—and the more prepared you are, the better.

FAQs

What is an example of AMT?

Consider a taxpayer who exercises Incentive Stock Options (ISOs) to purchase 100 shares at $3 per share when the market price is $10 per share. Under regular tax rules, the income from this transaction isn't recognized until the shares are sold. However, for AMT purposes, the "bargain element"—the difference between the exercise price and the market value—is added to income in the year of exercise. This adjustment can increase the Alternative Minimum Taxable Income (AMTI), potentially triggering AMT liability.

How do I find my alternative minimum tax?

To determine if you're subject to the AMT, complete IRS Form 6251, "Alternative Minimum Tax—Individuals." This form guides you through adjustments and preferences that differ from regular tax calculations, helping you compute your AMTI. After calculating your tentative minimum tax, compare it to your regular tax liability. If the tentative minimum tax exceeds your regular tax, the difference is your AMT liability.

What form do I use to calculate alternative minimum tax?

To calculate the AMT, use IRS Form 6251, "Alternative Minimum Tax—Individuals." This form helps you determine your AMTI by accounting for specific adjustments and preferences. It then calculates the tentative minimum tax, which you compare to your regular tax to ascertain any AMT owed.

What income level triggers the alternative minimum tax?

The AMT exemption amounts vary by filing status and are adjusted annually for inflation. For the 2024 tax year, the exemptions are:

- Single or Head of Household: $81,300

- Married Filing Jointly or Qualifying Widow(er): $126,500

- Married Filing Separately: $63,250

These exemptions phase out at higher income levels, starting at $578,150 for single filers and $1,156,300 for married couples filing jointly. Taxpayers with incomes above these thresholds may be subject to the AMT.

How to avoid paying alternative minimum taxes?

To minimize or avoid AMT liability, consider the following strategies:

- Timing Deductions and Income: Defer or accelerate income and deductions to years when you're less likely to be subject to the AMT.

- Manage Incentive Stock Options (ISOs): Exercise ISOs strategically to control the timing of income recognition for AMT purposes.

- Review Tax-Exempt Interest: Be cautious with private activity municipal bonds, as their interest is taxable under AMT rules.

Consulting a tax professional can provide personalized strategies based on your financial situation.

By understanding the intricacies of the AMT and implementing effective tax planning, you can reduce the likelihood of unexpected tax liabilities.

About the Author

This article was written by Rohit Kapoor, Co-founder of Accounti. With over 20 years of experience in leading finance operations at global organizations such as Credit Suisse and Capgemini, I bring expertise in financial operations, management reporting, and finance transformation. As a Chartered Accountant, my focus is on simplifying complex financial processes, enhancing efficiency, and implementing scalable solutions that support the growth of businesses. My approach combines strategic insight with hands-on execution to deliver sustainable financial frameworks for organizations across industries.